.svg)

Lending Intelligence

SBA 7(a) Loan Trends: Key Q3 FY2025 and YoY Insights

The landscape of small business lending in FY2025 reveals a dynamic shift shaped by regulatory updates and evolving borrower needs. Data from the Small Business Administration (SBA) highlights a year marked by fewer loan approvals but larger average loan sizes, driven in part by the SOP 50 10 8 policy update that tightened underwriting standards and eligibility requirements mid-year.

This environment has encouraged more prudent stewardship of SBA funds, ensuring that capital reaches financially resilient businesses. Notably, startups secured the highest average loan amounts—33% greater than established firms—while mature businesses accounted for the majority of approvals. Geographic trends show California and Texas leading in both loan volume and funding, with rural borrowers consistently outpacing urban peers in both approvals and average loan size. Across industries, construction led in loan count, while Accommodation and Food Services received the most funding dollars.

Annual data from 2021 to 2025 further underscores a reversal in trend: Loan count decreased year over year for the first time in recent history.

These insights signal a significant shift in dynamics of the SBA market and emphasize the importance for lenders to refine strategies, embrace digital platforms, and expand outreach to better serve the evolving small business community profitably.

Looking at the 2025 fiscal year quarter over quarter, the data tells a primary story: fewer approvals, larger sizes. The primary influence for this trend is likely the Small Business Administration’s SOP 50 10 8 policy update that took effect on June 1, 2025, tightening lending practices for the end of Q3 and entirety of Q4.

This policy change enacted stricter regulations around underwriting standards, eligibility requirements, and equity injection conditions. These guidelines encourage more mindful stewardship of the SBA program, making these funds available to more small business owners for years to come.

We look at lending trends by borrower segment below, but here’s a snapshot of FY2025 according to this year’s data:

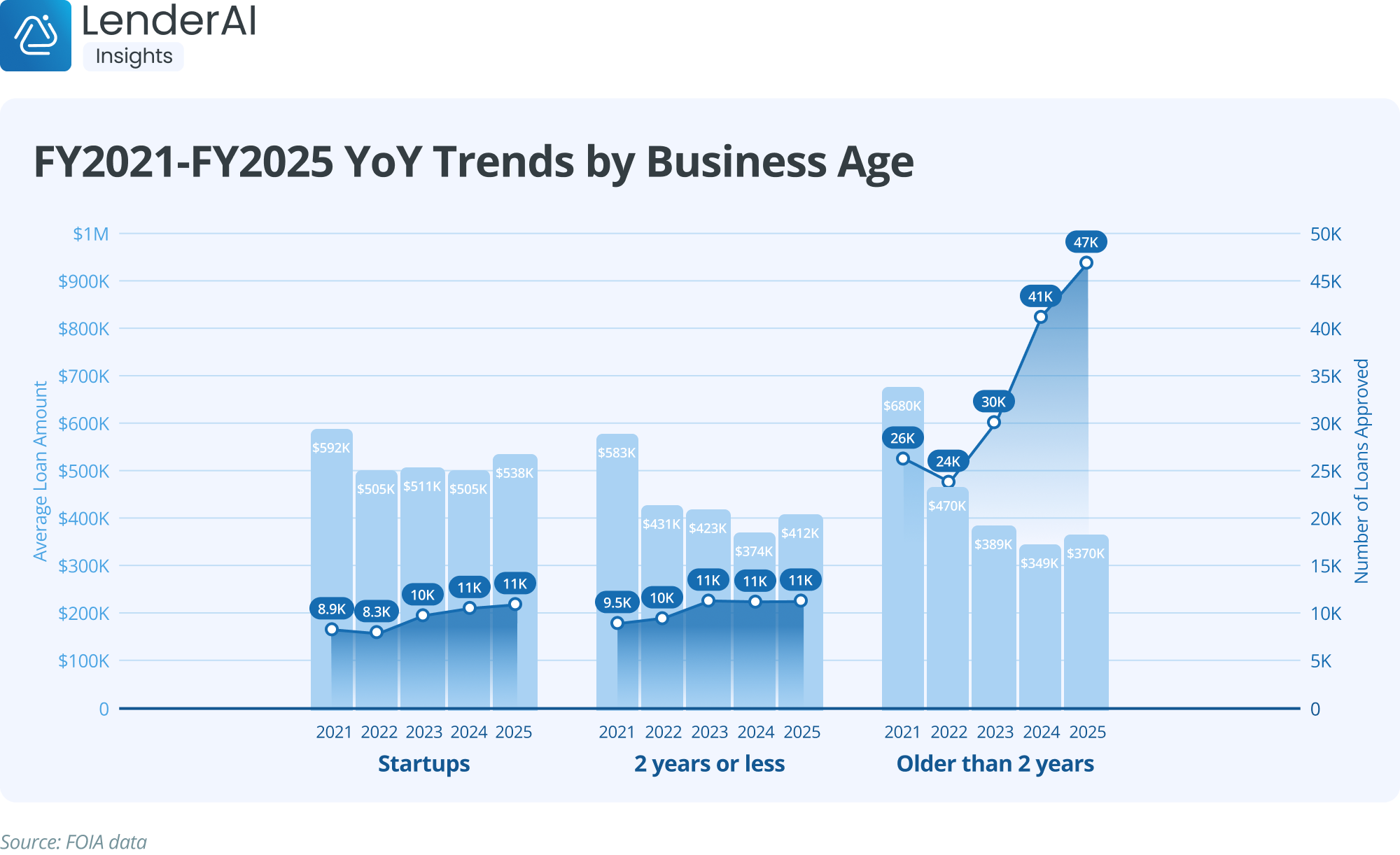

We first looked at the past fiscal year’s lending trends by business age. As expected given June’s SOP change, total loan count declined from Q2 to Q4, while average loan size increased. It’s likely that the SBA’s SOP change impacted the number of applicants who met new eligibility requirements.

Established businesses two years or older were approved for the most loans at a dramatic increase over younger businesses. However, it was startups that were approved for the highest loan amounts, 33% more than established businesses. These trends could simply indicate how startups need more working capital to get their businesses up and running, while more established businesses are more eligible to meet changing credit requirements.

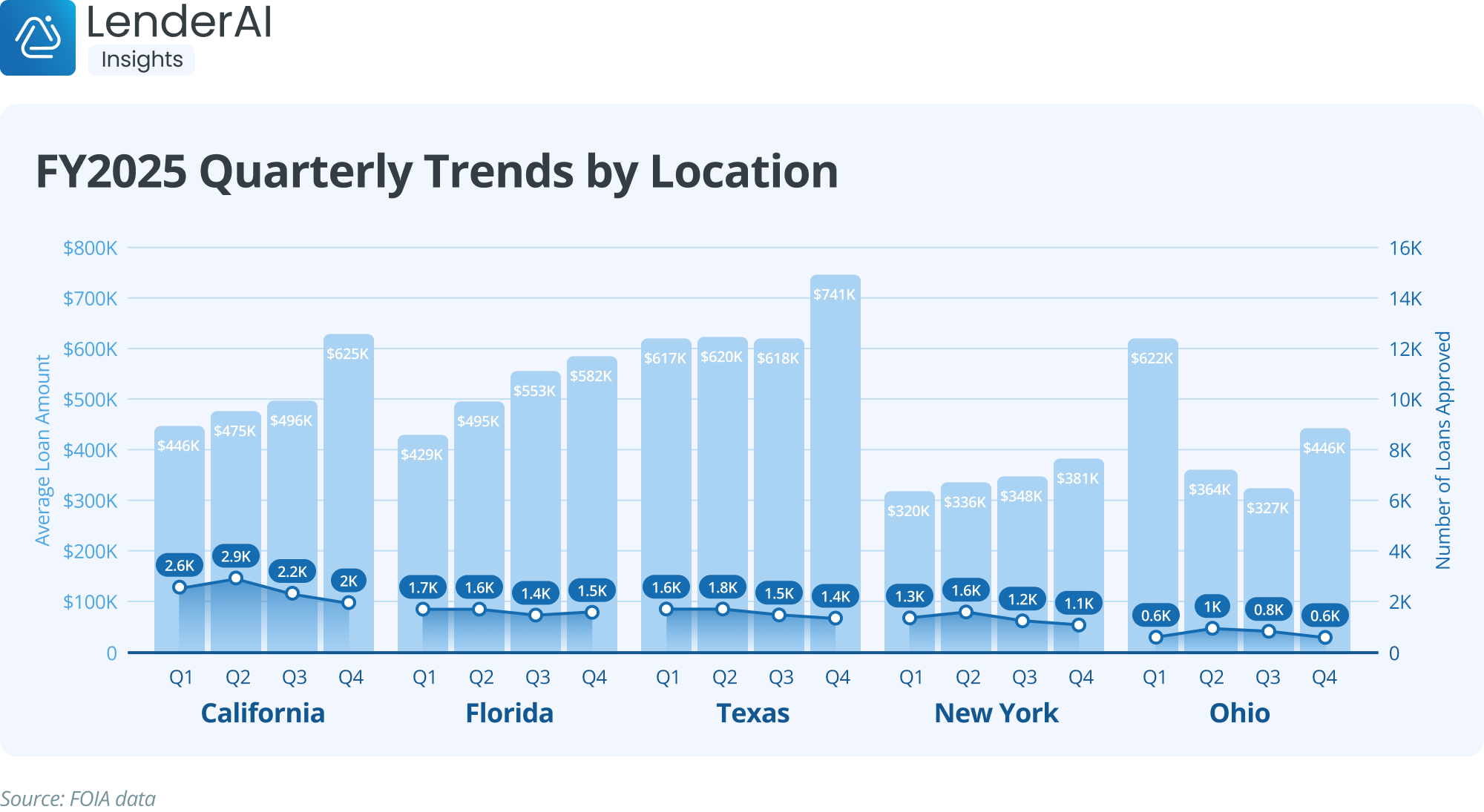

Next, we looked at the year’s lending trends across the country, focusing on the states that received the largest percentage of SBA funding in FY2025. As with the previous segment, small business lending statistics by location showed an increase in loan size and decrease in loan count quarter to quarter, with only one state breaking from the theme.

SBA demographics data shows that California dominated loan funding, accounting for roughly 13% of both loan approvals and dollar amounts across all states, with Florida not far behind at 8.5%. Both states’ major industries span agriculture, manufacturing, construction, technology, real estate, and health care—providing job opportunities and regional economic boosts across many diverse sectors in these states.

The numbers trended much the same when we used Metropolitan Statistical Area (MSA) codes to identify loan characteristics among rural and urban small businesses. At first glance it may seem that urban businesses would receive a larger percentage of funding due to greater population and businesses per capita, but SBA loan data shows that rural borrowers consistently secured more approvals and higher funding amounts in FY2025. Though we see the same Q3 pull-back as we do in other segments, rural borrowers had 43% more approved loans than urban in the 2025 fiscal year and a 5% greater average loan size.

This could be due to rural business owners relying more heavily on SBA programs thanks to its outreach in these less populated areas, such as USDA and other SBA programs that support rural businesses.

Lastly, we looked at the industries that received the greatest percentage of SBA funding for the fiscal year. Again, the year’s key trends are fewer but larger loans as the year progresses and a Q3 drop in loan count. The construction industry led in loan count at 13.6% of total loan approvals across all industries. Accommodation and Food Services received the most funding over the last fiscal year, however. This industry made up 16.4% of SBA dollars approved.

Year over year, SBA lending data shows fluctuation from 2021 to 2025, but lending trends for this five-year period are largely reversed from what we see for the 2025 fiscal year. Whereas in FY2025 loan count decreased and average approved loan amount rose over time, FY2021 to 2025 small business lending data shows loan count trending upward and dollar amount primarily going down year over year.

As we break down the year-over-year trends by segment below over the last five fiscal years, the following influences are at play:

Loan trends by business age reflect the sentiment above: More loans were approved year over year but for less capital. The data shows that startup lending remained more consistent compared to that of more mature businesses both in loan count and average loan size, despite tightening credit standards.

In early 2025, the SBA released a report highlighting that the number of small business applications between January 2021 and January 2025 totaled 21 million, an average of more than 440,000 applications per month, which is more than 90% greater than pre-pandemic averages. Lenders can capture the loyalty of these emerging businesses early by offering convenient digital application experiences and quicker access to capital.

SBA data indicates that established businesses, those operating for two years or more, account for the majority of loan approvals. At the same time, the average approved loan amount has declined, even as total approvals have increased. This combination suggests a shift in the composition of loan activity: more established firms are securing financing, but the financing they receive tends to be smaller in dollar value. The observed pattern looks consistent with the financing behavior typically seen as businesses mature, where SMB capital needs often become more incremental rather than foundational.

Looking across the top-funded states, the continuing trend stands out. Loan counts increase each fiscal year from 2021 through 2025, even as average loan amounts settle back to more typical levels after the unusually high peaks seen in 2021. While California saw the most loans approved over this five-year window, it was Texas that was approved for the most funding—10.7% of all SBA funding in the country.

Both rural and urban areas have seen tremendous growth in borrower participation over the last five years, but rural borrowers far outpaced urban regions in loan count. In rural regions, SBA loan approvals climbed nearly 40% from 2021 to 2025. Though average rural and urban funding amounts have remained comparable since 2023, the number of approved loans is drastically different. Even in the year with the fewest approved loans (2022), rural borrowers still saw over double the approvals as urban.

While average loan sizes have declined from pandemic-era highs in 2021, the most-funded industries still show significant growth in loan count, with year-over-year increases across key sectors. The year-over-year data we see across these industries shows steady borrower participation in SBA funding even as average loan sizes stabilize. Lenders who modernize their processes and technology to provide efficient, convenient borrower experiences will be better positioned to support the increasing application rates we’ve seen over the last year.

While the most recent FOIA report does not include quarterly SBA loan data for racial demographics, the SBA’s 7(a) program summary report provides a look at year-over-year small business loan trends by race. From 2021 to now, every racial demographic represented has experienced an increase in loan approvals. Minority business owners saw a particularly steep incline in loan count, with Hispanic- and Black-owned businesses roughly doubling approved applications.

By 2025, each demographic settled into a more sustainable average loan size as seen in other segments. One of the most notable new trends, however, is the growing number of borrowers who did not report race, increasing from 11,849 in 2021 to more than 21,000 in 2025.

Overall, the data from fiscal year 2025 shows the following:

Year over year, we see the following:

What can lenders do with these insights? First, we suggest using this data and tools like LenderAI Insights to finetune your lending strategy. Consider these tips:

It's increasingly important for lenders to make the most of SBA funding. This comes from both the need to steward funds more mindfully among changing regulations, as well as the growing demand for SBA support from borrowers. The clearest action items are to refine lending strategies, increase outreach, and tailor offerings to reach and fund as many small business owners as possible as wisely as possible.

One way financial institutions can serve more borrowers and better manage their lending programs is to invest in tools that help them optimize how they work. End-to-end small business lending software like LenderAI streamline your loan operations so your team can efficiently manage more loans while also providing borrowers the modern, digital application experience they expect.

Emerging software development platforms like iBuild utilize AI’s vibe-coding capabilities to enable even non-technical lending teams to create business applications. Lending teams can design, build, and deploy products in minutes—empowering your team to build its own tools without writing a single line of code.

Schedule a demo of either tool to see how these platforms can help lenders like you grow, and stay informed of industry trends by creating a free LenderAI Insights account.

.png)

.png)

.png)

.svg)