.svg)

Lending Intelligence

FY2025 SBA Loan Data Trends: Analysis and Insights for Lenders

While FY2025’s year-over-year lending numbers began strong, recent SOP changes from the Small Business Administration have had a measurable impact on Q3. However, the influence of SOP updates may not be as dramatic as some lending professionals believed, with the latest FOIA and LenderAI Insights data indicating that FY2025 is still pacing well and is on track to end with continued growth over FY2024.

Below, we examine what this data highlights about Q3 FY2025, which borrower profiles are getting approved the most despite stricter requirements, and where lenders have the opportunity to serve more borrowers while complying with changing SOPs.

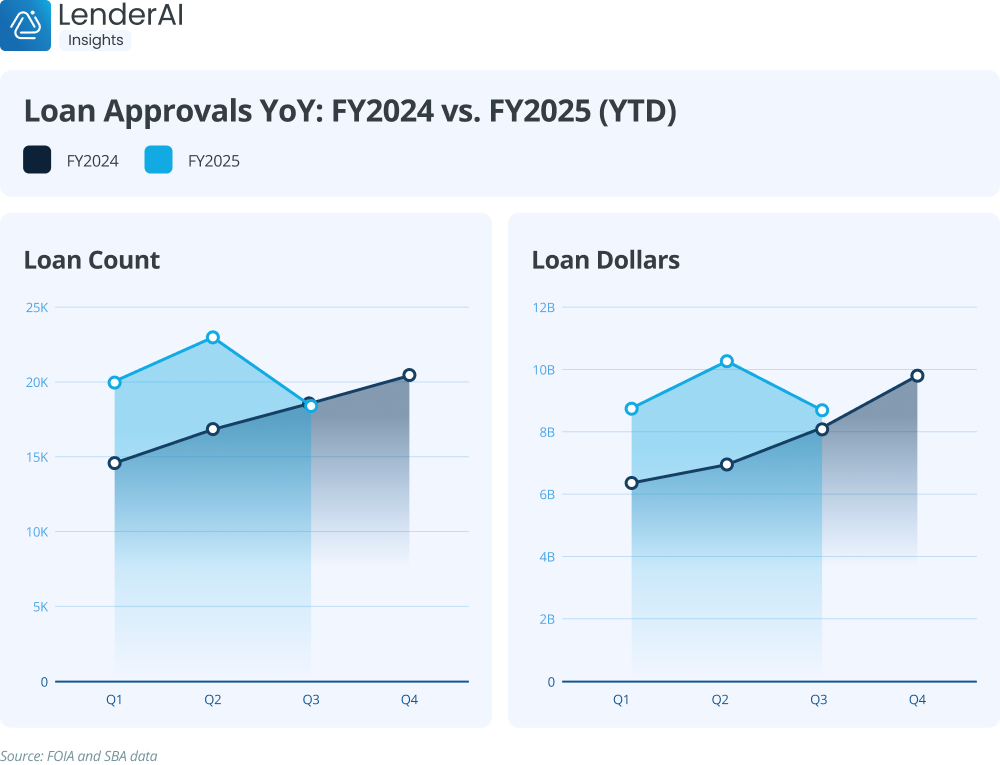

Loan volume and approved dollars saw the usual dip from Q4 FY2024 to Q1 FY2025 but steadily rose from Q1 to Q2, showing a healthy year-over-year increase. The pace didn’t continue in Q3 FY2025, however. While both metrics experienced a 14% to 16% jump quarter to quarter at the start of the fiscal year, we saw a 17% to 22% decline in Q3.

Why the Q3 dip? As expected, the Small Business Administration’s SOP 50 10 8, which took effect on June 1, 2025, tightened lending practices for the final month of Q3. Though the quarter’s numbers trend down, this SOP change has positive effects.

SOP 50 10 8 includes tighter underwriting standards, stricter eligibility requirements, and higher equity injection conditions. These tighter regulations mean applicants getting funded are stronger and have less financial risk, which makes SBA loan programs more viable and better utilized long-term. Cautious stewardship of the SBA program means more businesses will be able to access this funding for years to come. It also results in stronger loans that strengthen lenders’ portfolios.

While we’ve seen a slight quarter-to-quarter dip this fiscal year, year-over-year growth is still healthy. Loan volume in Q3 FY2025 saw only a small drop from FY2024, and loan dollars actually rose this Q3 compared to last year. These numbers indicate a strong FY2025 overall.

Though Q3 numbers show the impact of recent SOP changes for some metrics, loan size is one area where we saw an increase. Loan sizes experienced no major change from Q1 FY2025 to Q2 but had a roughly 6% increase in Q3. Fewer borrowers may be meeting new SOP requirements, but larger loan sizes are being approved for those that qualify.

.png)

In fact, large SBA 7(a) loans make up over half of the approved lending dollars this fiscal year, totaling just over $10 billion. This may indicate that lenders are prioritizing larger loans to small businesses with more established financials, rather than funding more loans of varying sizes. This presents an opportunity for institutions like community banks and CDFIs to ensure smaller businesses with smaller capital needs are still effectively served.

We looked at the latest SBA demographics data to examine trends in key areas for FY2025 through the end of Q3 compared to FY2024. Despite recent SOP changes, this year is on track to finish with higher approval counts in all segments, with many FY2025 borrower profiles already exceeding total FY2024 numbers.

Construction, Food Service, and Retail industries lead FY2025 approvals to date, with Food Services being approved for the largest loan sizes year over year. The Health Care and Social Assistance industries and those related to Professional, Scientific, and Technical Services have seen the most growth in FY2025, already exceeding the total FY2024 approval count and average loan size by roughly 2%. Data shows that the top borrowing industries year over year are on pace to exceed last year’s approved loan count and size, with the top five industries ending Q3 just 3.6% behind the total FY2024 numbers.

.png)

With one quarter left in the fiscal year, data shows that minority business owners are on pace to exceed FY2024 approval numbers. Hispanic, Asian, Black, American Indian, and Alaska Native borrowers ended Q3 an average of only 10% behind their total FY2024 approval counts. Similarly, primarily female-owned businesses ended Q3 just under 10% behind their FY2024 approval numbers.

.png)

We looked at loan approval counts across the different SBA categories for business age, type, and size as well as rural and urban business locations. For all segments, we found that this year’s numbers have either already exceeded FY2024 or are only 2% to 6% lower than FY2024 with one quarter left to go.

Given the stricter qualifying requirements due to June’s SOP change, we expected established businesses to have a distinctly higher loan approval count than younger businesses. However, Q3’s dip doesn’t show up as much as anticipated when looking at business age. While businesses over two years old have already exceeded FY2024 counts, startups and businesses two years old or younger are less than 6% behind the prior year’s totals.

.png)

Though Q3 FY2025 approval numbers decreased from Q2, this fiscal year as a whole still shows long-term strength. After seeing the latest data, here’s what lenders may want to keep in mind:

Given FY2025’s pacing and the trend of many businesses applying for funding at the start of Q4 in preparation for the holiday season and the new year, we expect this fiscal year to finish above FY2024 in both approvals and loan dollars. Despite a Q3 slowdown, the year-to-date trajectory is positive. Loan dollars are up, demographic segments are resilient, and the SBA program is better positioned for long-term sustainability. For lenders, this means FY2025 won’t just be a strong year; it has the ability to reshape portfolios for greater health and resilience.

SOP changes may have slowed approvals in the short term, but they’re creating a healthier, more sustainable lending environment. As we wrap up FY2025, the key challenge for banks and lenders is to balance adherence to SOP guidelines with a focus on ensuring that the range of small business owners are well-served.

One way lenders can manage SBA compliance while addressing more loans and serving more small business owners is having the right lending tools. LenderAI optimizes loan origination from sales through servicing, allowing lenders to automate manual tasks, make smarter and more thorough decisions, and better assess risk, all while improving communication with borrowers and helping navigate the complexities of changing SOPs.

Learn more about LenderAI and schedule a demo to see how our platform can help lenders like you grow.

.png)

.png)

.png)

.svg)